In this case, the truth is the library has started an insurance fiction collection. The University of Connecticut School of Law is already ahead of us in this respect, but we're starting to play catch up. Our Director, Jean Lucey, has wanted to start a fiction section since Sue Grafton's mystery series starring Kinsey Milhone, former investigator for California Fidelity Insurance, came out. Last Christmas she got her wish when all of the "alphabet series" was added to the collection (U is for Undertow had just been published).

This year, a few more books were added to the collection including, The Pale Green Horse, Horse Sense, Bet Your Life and Bringing Back Eight: A Novel about Medical Malpractice on Trial. We've also added our first dvd to the collection, Memento. We encourage you to come in and read or check out some of our newest additions.

If you have suggestions for the fiction section, we welcome your feedback (either via a comment on this blog post or email). We also welcome donations either to our fiction section or to our general collection. If you're looking for ideas on books that we're especially interested in, please peruse our amazon wish list.

Wednesday, December 29, 2010

Tuesday, December 21, 2010

The Whole Pie

The Massachusetts Attorney General publishes a Report on Professional Solicitations for Charities annually. This year's report has caused a stir (at least in the Boston Globe) since it reports that charities received only 43% of the money that was raised; the rest went to the professional fundraisers.

Last year New York's Attorney General brought a case against four professional fundraising telemarketers who employed deceptive and unfair tactics. These deceptive tactics included in some cases lying about how much of the money the charity would receive. It turned out, on average, these professional fundraisers were keeping 76% of the money they raised.

All is not lost though, there are various ways that one can determine the amount a charity will receive. Sometimes this information is right on the charity's website. You can also ask for the information from the telemarketer in writing. Finally, checking to see if the fundraiser is a member of the Association of Fundraising Professionals can help. This association has a code of ethics to which they ascribe.

Another way to determine generally how much of the money you give to a charity goes toward furthering their mission is to check a website like Charity Navigator. It will give you and idea of the charity's organizational efficiency, organizational capacity as well as an income statement usually including how much the ceo is paid.

We thought that this might be a timely post considering the recent series of Boston Globe articles on the topic. We want to assure you that our library does not use professional fundraisers. As we mentioned in a past post, we are a non-profit and there are a number of ways that you can donate to the library before the end of the year. The most direct way is probably through our annual fund, which you can donate to by clicking here.

Last year New York's Attorney General brought a case against four professional fundraising telemarketers who employed deceptive and unfair tactics. These deceptive tactics included in some cases lying about how much of the money the charity would receive. It turned out, on average, these professional fundraisers were keeping 76% of the money they raised.

All is not lost though, there are various ways that one can determine the amount a charity will receive. Sometimes this information is right on the charity's website. You can also ask for the information from the telemarketer in writing. Finally, checking to see if the fundraiser is a member of the Association of Fundraising Professionals can help. This association has a code of ethics to which they ascribe.

Another way to determine generally how much of the money you give to a charity goes toward furthering their mission is to check a website like Charity Navigator. It will give you and idea of the charity's organizational efficiency, organizational capacity as well as an income statement usually including how much the ceo is paid.

We thought that this might be a timely post considering the recent series of Boston Globe articles on the topic. We want to assure you that our library does not use professional fundraisers. As we mentioned in a past post, we are a non-profit and there are a number of ways that you can donate to the library before the end of the year. The most direct way is probably through our annual fund, which you can donate to by clicking here.

Wednesday, December 15, 2010

Burning Interest in Punitive Damages

In Massachusetts yesterday a jury awarded 71 million dollars when they found a tobacco company liable for the death of Marie Evans. The full story can be found in the Boston Globe, among other places. It turns out that the tobacco company in question, "Lorillard had never lost a case brought by an individual before yesterday" While the tobacco company is appealing the case, there is speculation that more cases may follow as a result of this one.

Apparently "the verdict sets up a second phase of deliberations in which the jury could also award Evans’s estate and family punitive damages, which often are a multiple of the amounts awarded in the compensatory phase." Insurance coverage for punitive damages is actually an interesting topic. By interesting, I mean it is a topic that is worthy of many articles full of discussion as well as a few books. Clearly we don't have the space to explore all of the ramifications here in a little blog post, but a section from The Thomson West Publication: Punitive Damages Law and Practice by John J. Kircher and Christine M. Wiseman sheds some light on how convoluted a topic it is.

If you're interested in more information on punitive damages or products liability, please feel free to email the library with your specific question or stop by and check out our collection.

Apparently "the verdict sets up a second phase of deliberations in which the jury could also award Evans’s estate and family punitive damages, which often are a multiple of the amounts awarded in the compensatory phase." Insurance coverage for punitive damages is actually an interesting topic. By interesting, I mean it is a topic that is worthy of many articles full of discussion as well as a few books. Clearly we don't have the space to explore all of the ramifications here in a little blog post, but a section from The Thomson West Publication: Punitive Damages Law and Practice by John J. Kircher and Christine M. Wiseman sheds some light on how convoluted a topic it is.

The question of insurance coverage for punitive damages continues to plague the courts, insurers, and insureds. The trend appears to favor finding coverage, but the decisions have not persuasively decided the issue. In fact, they have more recently enhanced the controversy by positing additional arguments both in support of and in opposition to coverage. (pp 7-38-7-39)

They go on to discuss the reasoning behind punitive damages and explore whether insurance coverage hinders those motives:

In most jurisdictions, punitive damages are intended to be awarded not to compensate the injured, but to punish the wrongdoer and to deter the wrongdoer and others from similar egregious conduct. Once it is determined that punitive damages are covered by the policy terms, courts then face the issue whether coverage would frustrate the public policy involved in the punishment and deterrence considerations of the punitive damages. (pp 7-42-7-43)

If you're interested in more information on punitive damages or products liability, please feel free to email the library with your specific question or stop by and check out our collection.

Thursday, December 9, 2010

Vertically Challenged

We noticed in the stats section of our blog, that some people had happened upon our blog using the search terms "vertical liability." Turns out we're third from the top on the Google search for that term because of our brief post on products liability where we mentioned that we had vertical files with subject information.

Unfortunately, I am not sure exactly what the searchers were looking for. The term vertical liability is not, as far as I know, standard language in insurance. One possibility for what might be of interest is supply-chain liability. In other words, what is the liability for the person up or down the chain if there's been a loss at some point in the chain. While I am sure we could provide more information on the topic, if pressed, it seems like the best plan is to try and avoid losses like this in the first place. As it says on the Risk and Insurance Management Society website: "supply chain management can stop supplier issues from becoming your own." To this end, Risk Management Magazine published an article in their April edition titled: How Spend Analysis Can Reduce Supply Chain Risk: Domino effect They also had a great article in August of 2008 entitled: Understanding Supply Chain Risk which included helpful flow charts.

Another possible topic of interest might have been vertical exhaustion of limits which has to do with the interaction of primary policies and excess or umbrella insurance policies. Vertical exhaustion of limits is described in a July 2002 article in Defense Counsel Journal as such: "vertical exhaustion allows an insured to seek coverage from an excess insurer as long as the insurance policies immediately beneath that excess policy, as identified in the excess policy's declaration page, have been exhausted, regardless of whether other primary insurance may apply." It turns out that vertical exhaustion of limits is actually somewhat controversial. Most case law appears to support horizontal exhaustion of limits, which requires exhausting the limits of ALL primary insurance which might apply before an insured can turn to his excess policies. The Defense Counsel Journal article described above and entitled Excess-Primary Insurer Obligations and the Rights of The Insured by Thomas M. Hamilton and Troy A. Stark addresses this issue quite well. For more up to date information on the topic, you might try getting your hands on a Donald Malecki article from the December 2008 edition of Malecki on Insurance entitled Horizontal Versus Vertical Exhaustion of Limits (found in a subscribers forum issue). He provides case law from 2007 and 2008 on the topic as well as his expert opinion.

While we'll continue to look at the stats for possible areas of interest, we also welcome suggestions for future blog posts. You can email the library or post a comment!

Unfortunately, I am not sure exactly what the searchers were looking for. The term vertical liability is not, as far as I know, standard language in insurance. One possibility for what might be of interest is supply-chain liability. In other words, what is the liability for the person up or down the chain if there's been a loss at some point in the chain. While I am sure we could provide more information on the topic, if pressed, it seems like the best plan is to try and avoid losses like this in the first place. As it says on the Risk and Insurance Management Society website: "supply chain management can stop supplier issues from becoming your own." To this end, Risk Management Magazine published an article in their April edition titled: How Spend Analysis Can Reduce Supply Chain Risk: Domino effect They also had a great article in August of 2008 entitled: Understanding Supply Chain Risk which included helpful flow charts.

Another possible topic of interest might have been vertical exhaustion of limits which has to do with the interaction of primary policies and excess or umbrella insurance policies. Vertical exhaustion of limits is described in a July 2002 article in Defense Counsel Journal as such: "vertical exhaustion allows an insured to seek coverage from an excess insurer as long as the insurance policies immediately beneath that excess policy, as identified in the excess policy's declaration page, have been exhausted, regardless of whether other primary insurance may apply." It turns out that vertical exhaustion of limits is actually somewhat controversial. Most case law appears to support horizontal exhaustion of limits, which requires exhausting the limits of ALL primary insurance which might apply before an insured can turn to his excess policies. The Defense Counsel Journal article described above and entitled Excess-Primary Insurer Obligations and the Rights of The Insured by Thomas M. Hamilton and Troy A. Stark addresses this issue quite well. For more up to date information on the topic, you might try getting your hands on a Donald Malecki article from the December 2008 edition of Malecki on Insurance entitled Horizontal Versus Vertical Exhaustion of Limits (found in a subscribers forum issue). He provides case law from 2007 and 2008 on the topic as well as his expert opinion.

While we'll continue to look at the stats for possible areas of interest, we also welcome suggestions for future blog posts. You can email the library or post a comment!

Tuesday, November 30, 2010

More Holiday Fire Talk

We were sort of a killjoy when it came to Thanksgiving. We're back to talk about Chanukah which starts this week (sundown on the 1st if I read my calendar right). You're probably thinking we'll harp on how dangerous frying food is, or how having 9 candles burning near wrapping paper is a definite no-no. You'd be wrong though. What we have to talk about today is only tangentially related to Chanukah.

Recently I was looking at the definition of fire in an insurance glossary (Rupp's Insurance and Risk Management Glossary, 2nd edition for those of you who don't follow the link). I thought it was very interesting that the glossary differentiated between friendly fire and hostile fire especially since I had really only heard the term friendly fire in regard to war.

In insurance terms, Chanukah candles would epitomize friendly fire. They are set intentionally for beneficial purposes and (it is hoped) remain within their intended confines. Insurance does not cover friendly fire unless it spreads to unintended materials (in other words, becomes hostile).

If you are yearning for more information on fire definitions, you'd probably like to know that most fires caused by modern Chanukah celebrations would be considered "class a fires," fires involving solid combustibles and best put out using water or class a fire extinguishers. Had the oil lamp at the original Chanukah spread beyond the proper confines, it would have been a "class b fire," a type of fire involving flammable liquids (oil) and requiring carbon dioxide or a class b fire extinguisher to put out.

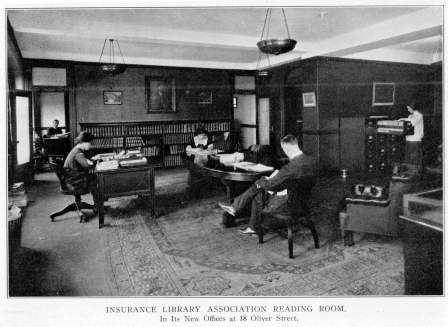

My foray into the insurance glossary section of our collection led me to an 1886 book called Harris's Technical Fire Insurance Dictionary. As you may know, our library began in 1887 as a fire insurance library (we didn't add casualty insurance to our collection until 1920 and it wasn't until the 1970s that we broadened our collection to include life and health insurance). This means, that the book was part of our very early collection housed in this room:

And carefully watched over by a librarian following these rules:

My favorite entry in the book though, is the following:

Recently I was looking at the definition of fire in an insurance glossary (Rupp's Insurance and Risk Management Glossary, 2nd edition for those of you who don't follow the link). I thought it was very interesting that the glossary differentiated between friendly fire and hostile fire especially since I had really only heard the term friendly fire in regard to war.

In insurance terms, Chanukah candles would epitomize friendly fire. They are set intentionally for beneficial purposes and (it is hoped) remain within their intended confines. Insurance does not cover friendly fire unless it spreads to unintended materials (in other words, becomes hostile).

If you are yearning for more information on fire definitions, you'd probably like to know that most fires caused by modern Chanukah celebrations would be considered "class a fires," fires involving solid combustibles and best put out using water or class a fire extinguishers. Had the oil lamp at the original Chanukah spread beyond the proper confines, it would have been a "class b fire," a type of fire involving flammable liquids (oil) and requiring carbon dioxide or a class b fire extinguisher to put out.

My foray into the insurance glossary section of our collection led me to an 1886 book called Harris's Technical Fire Insurance Dictionary. As you may know, our library began in 1887 as a fire insurance library (we didn't add casualty insurance to our collection until 1920 and it wasn't until the 1970s that we broadened our collection to include life and health insurance). This means, that the book was part of our very early collection housed in this room:

(taken from the 1923 edition of The Insurance Index)

And carefully watched over by a librarian following these rules:

A larger version of this can be found by following this link.

Harris's Technical Fire Insurance Dictionary has many interesting entries. The preface states:This book, comprising in a condensed form many notes and observations made by the Author during a long and very busy experience as Surveyor, Inspector and Branch Secretary, has been written mainly with the view of drawing attention of Fire Insurance Officials and Agents to important points connected with matters of survey, and general practice and to the many dangers arising not only during processes of manufacture, but also from the crowded character of risks; from spontaneous combustion; and from other sources too numerous to mention.Yes, all of that is one sentence, and also the first paragraph of the preface! I love that it includes this phrase: "comprising in a condensed form. . ." leaving me to wonder what a fully expanded form would look like.

My favorite entry in the book though, is the following:

If you are as charmed by this book as I am or there's someone on your holiday list who you think might be taken with it, feel free to contact us about the possibility of adopting the book as part of our "adopt a book" program. While the book is not in terrible shape, it could use some loving care to bring it back to its former glory.FIRES, Refreshments at: Bills for expenses of this kind require very careful scrutiny, and in no case should they be paid when refreshments have been given away indiscriminately, or without proper authority. In no case where publicans throw open their houses should any payment be authorised by the Agent. See also FIRES, Assistance At.

Friday, November 26, 2010

Black Friday

While I am one of those "shop through the year for holiday gifts" people, I admit I also get up to face the throngs on Black Friday. I would hate to be six days into those 8 crazy nights or stuck on December 23rd (yes, I celebrate both holidays) praying to the postal gods that the shipment will make it in the (st.) nick of time time.

Because today is such a huge shopping day for so many people, I thought it would be an appropriate time to let you know how you could remember the library while doing your holiday shopping. We have three main options for gifts to the library.

The Annual Fund is where general monetary donations throughout the year go. The money is spent on up-keep of the library as well as focusing on one or two projects for the year. Companies and individuals who donate to the annual fund get their name published in our newsletter (we're a non-profit so your donation may also be eligible for a tax deduction -- we're not tax experts though). This spring, the library had a flood so a good portion of the Annual Fund money was spent helping us recover.

Another way of supporting the library and its collection is through the "Adopt A Book Program" which provides for preservation of our historical publications and documents. The money donated goes toward a specific item --you can read some background about the books and look at them online in their tattered state to pick which one you want to adopt. We make sure a personalized book plate is put in the front, so users know whose generosity ensured future use of the material. The book plate can be donated in honor of someone in case you want to buy it as a gift for someone else. Your recipient can come into the library any time they want and admire the book-binder's handiwork and their name emblazoned on the inside cover.

Finally, the library has an Amazon Wishlist. While you're completing your other shopping on amazon, you can click over and skim the list. If anything catches your fancy, you can simply add it to your cart with the rest of your purchase and Amazon should know to send it to us. You'll notice there are items on the list for general office upkeep. We're currently using the 2004 version of Quicken and would love to upgrade to the 2011 version. We also have a laptop computer on the list. Our instructors muddle along on our current one which hasn't been replaced in a number of years and no longer has a working CD-Rom drive. As you would expect, the rest of the list is filled out with books. Many of these books have been requested by patrons or are for very specialized areas of insurance interest but aren't in our budget. If you find something that falls within your particular area of interest, we'd love it if you'd donate it to our library so we could share it with many more people.

We appreciate the many ways in which individuals and companies show their support for the library and hope that this information makes that support easier.

Because today is such a huge shopping day for so many people, I thought it would be an appropriate time to let you know how you could remember the library while doing your holiday shopping. We have three main options for gifts to the library.

The Annual Fund is where general monetary donations throughout the year go. The money is spent on up-keep of the library as well as focusing on one or two projects for the year. Companies and individuals who donate to the annual fund get their name published in our newsletter (we're a non-profit so your donation may also be eligible for a tax deduction -- we're not tax experts though). This spring, the library had a flood so a good portion of the Annual Fund money was spent helping us recover.

Another way of supporting the library and its collection is through the "Adopt A Book Program" which provides for preservation of our historical publications and documents. The money donated goes toward a specific item --you can read some background about the books and look at them online in their tattered state to pick which one you want to adopt. We make sure a personalized book plate is put in the front, so users know whose generosity ensured future use of the material. The book plate can be donated in honor of someone in case you want to buy it as a gift for someone else. Your recipient can come into the library any time they want and admire the book-binder's handiwork and their name emblazoned on the inside cover.

Finally, the library has an Amazon Wishlist. While you're completing your other shopping on amazon, you can click over and skim the list. If anything catches your fancy, you can simply add it to your cart with the rest of your purchase and Amazon should know to send it to us. You'll notice there are items on the list for general office upkeep. We're currently using the 2004 version of Quicken and would love to upgrade to the 2011 version. We also have a laptop computer on the list. Our instructors muddle along on our current one which hasn't been replaced in a number of years and no longer has a working CD-Rom drive. As you would expect, the rest of the list is filled out with books. Many of these books have been requested by patrons or are for very specialized areas of insurance interest but aren't in our budget. If you find something that falls within your particular area of interest, we'd love it if you'd donate it to our library so we could share it with many more people.

We appreciate the many ways in which individuals and companies show their support for the library and hope that this information makes that support easier.

Thursday, November 18, 2010

If You Can't Stand the Heat. . .

Not to be a debbie downer, but according to the National Fire Protection Association, "Thanksgiving is the peak day for home cooking fires." They have been proclaiming this on their website since at least 2006 (prior to that it appears that they warned of cooking fires in general during the holidays). The U.S. Fire Administration has some interesting facts posted on their website regarding home cooking fires. These facts were gleaned from a co-sponsored study with the NFPA. Highlights of the list are:

Grease Fires:

- Males face a disproportionate risk of cooking fire injury relative to the amount of cooking they do.

- Unattended cooking is the single leading factor contributing to cooking fires.

- Many other cooking fires begin because combustibles are too close to cooking heat sources.

- More than half of the home cooking injuries occur when people try to fight the fire themselves.

The Home Safety Council also has a convenient list of ways to prevent fires and fire injuries. Most of the fire safety tips are pretty common sense.

- Watch food at all times when you're cooking.

- Don't leave the house if you've got something in the oven or simmering.

- Don't cook when you're drowsy.

- Wear clothes that are close fitting so they don't accidentally ignite.

- Remove any combustible items from around the stove (eg: don't leave oven mitts near any burners).

- Keep your cooking area clean. Do not let grease build up on the range top, toaster oven or in the oven.

- Keep a lid handy to slide over a pan to smother a fire that might start.

Grease Fires:

- Should you have a grease fire on your stove top, smother the fire by sliding a lid over the pan and turn off the stove top. Leave the pan covered until the pan cools completely (opening the pan to check on it allows oxygen in which can re-ignite the fire).

- Never put water on a grease fire or use a multipurpose fire extinguisher on a pan fire, as it can spray or shoot burning grease around the kitchen, actually spreading the fire.

- Never attempt to carry a flaming pan across the kitchen.

Oven Fires:

- Turn off the heat and keep the oven door closed.

- Never open the door until the fire is completely out (allowing oxygen in can re-ignite the fire).

Microwave Fires:

- If you have a fire in your microwave, turn it off immediately and keep the door closed.

- If you can safely reach the outlet unplug the microwave oven.

- Never open the door until the fire is completely out (allowing oxygen in can re-ignite the fire).

- Have the microwave oven checked and/or serviced before being used again.

This is by no means an exhaustive list of cooking fire information. While we are not experts on fire safety, we have tried to compile some of the basic information here and provide you with sources (NFPA, The U.S. Fire Administration and the Home Safety Council) that can further your research into this topic. Remember, the most important advice regarding fighting kitchen fires is, When in doubt, just get out! Close the door behind you and call the fire department from outside.

We here at the library hope you have a happy and safe Thanksgiving holiday!

Wednesday, November 17, 2010

Annual Meeting Recap

This year's annual meeting was fairly eventful. We said a sad farewell to several of our trustees. Trusting that they'll remain stalwart library supporters.

Paula Gold Vice President and Chief Regulatory Counsel for Plymouth Rock Assurance, has been replaced by Charles (Chuck) C. Hewitt, III Executive Vice President of Guy Carpenter.

John Donohue CEO of Arbella has been replaced by Jim Hyatt, also of Arbella. In June, Jim Hyatt became the Vice President of their personal lines group.

Philip J. Edmundson, CEO and Chairman of William Gallagher Associates, who was brought on as an associate treasurer mid-term 1989 and then as a full board member as of the November 1989 meeting, also passed the torch. Patrick J. Veale, President of WGA, has taken Phil's place (he brought up some excellent points during the meeting and we're eager to see what other ideas he brings to the board).

Though his term was not up, Josiah D. Hatch, president of H. R. Hatch Insurance Agency, has stepped down. He was a special appointment to The Board in December of 1995. The Board voted to make him a Trustee Emeritus for all of his hard and exceedingly productive work over the past 15 years. A new Trustee will be appointed to fill Josiah's place.

Other changes to the board included the election of a new Board President, Donald F. Vose Vice President of The Andover Companies. He seems eager to become familiar with all of the committees and has already sat on an education committee meeting.

A good portion of the meeting was also devoted to discussing the many Massachusetts and New Hampshire insurance continuing education classes which the library provides and the future of those classes. This included highlighting our foray into webinars with "Coverage Review of the Business Auto Policy" slated to start in January. See our website for current and upcoming class listings!

Paula Gold Vice President and Chief Regulatory Counsel for Plymouth Rock Assurance, has been replaced by Charles (Chuck) C. Hewitt, III Executive Vice President of Guy Carpenter.

John Donohue CEO of Arbella has been replaced by Jim Hyatt, also of Arbella. In June, Jim Hyatt became the Vice President of their personal lines group.

Philip J. Edmundson, CEO and Chairman of William Gallagher Associates, who was brought on as an associate treasurer mid-term 1989 and then as a full board member as of the November 1989 meeting, also passed the torch. Patrick J. Veale, President of WGA, has taken Phil's place (he brought up some excellent points during the meeting and we're eager to see what other ideas he brings to the board).

Though his term was not up, Josiah D. Hatch, president of H. R. Hatch Insurance Agency, has stepped down. He was a special appointment to The Board in December of 1995. The Board voted to make him a Trustee Emeritus for all of his hard and exceedingly productive work over the past 15 years. A new Trustee will be appointed to fill Josiah's place.

Other changes to the board included the election of a new Board President, Donald F. Vose Vice President of The Andover Companies. He seems eager to become familiar with all of the committees and has already sat on an education committee meeting.

A good portion of the meeting was also devoted to discussing the many Massachusetts and New Hampshire insurance continuing education classes which the library provides and the future of those classes. This included highlighting our foray into webinars with "Coverage Review of the Business Auto Policy" slated to start in January. See our website for current and upcoming class listings!

Tuesday, November 16, 2010

The Frank W. Humphrey Award

The Frank W. Humphrey Golden Anniversary Award was established by Maurice H. Saval (after whom our education arm is named) in honor of Frank W. Humphrey, his mentor. Mr. Humphrey was at the agency Boit Dalton & Church, later Frank B. Hall & Company and now Aon Risk Services of Massachusetts. The prize was first awarded to commemorate Mr. Humphrey’s 50th year in the insurance business and is intended to be a special tribute to his contribution to our industry by his guidance and assistance to young people entering the business.

The winner each year is chosen from among those students who have successfully completed the course in Property and Liability Insurance Principles taught by Joe Sciacca. The student with the highest grade on the national exam that year earns the award. The presentation each year takes place during the Library's Annual Meeting.

This year's winner was Michelle Mozzicato from Crum & Forster. Michelle Mozzicato has worked at Crum & Forster Insurance for the past 11 years. She began her career with C&F as an Executive Assistant, and held that title for nine years. She was promoted to an Operations Supervisor in 2008, and most recently promoted to Operations Manager in 2009.

Prior to Crum & Forster Michelle was an Executive Assistant at BankBoston for 14 years. Michelle is married with two teenage boys, and resides in Stoneham, MA.

The picture below of Joe congratulating Michelle was taken by her husband at this year's meeting. You can expect more information on the annual meeting in tomorrow's blog post!

The winner each year is chosen from among those students who have successfully completed the course in Property and Liability Insurance Principles taught by Joe Sciacca. The student with the highest grade on the national exam that year earns the award. The presentation each year takes place during the Library's Annual Meeting.

This year's winner was Michelle Mozzicato from Crum & Forster. Michelle Mozzicato has worked at Crum & Forster Insurance for the past 11 years. She began her career with C&F as an Executive Assistant, and held that title for nine years. She was promoted to an Operations Supervisor in 2008, and most recently promoted to Operations Manager in 2009.

Prior to Crum & Forster Michelle was an Executive Assistant at BankBoston for 14 years. Michelle is married with two teenage boys, and resides in Stoneham, MA.

The picture below of Joe congratulating Michelle was taken by her husband at this year's meeting. You can expect more information on the annual meeting in tomorrow's blog post!

Joseph Sciacca & Michelle Mozzicato

Tuesday, November 9, 2010

Friday, November 5, 2010

We'll Trade

We'd like to take this opportunity to share with you some teaser photos from The Insurance Professional of the Year Award Ceremony (all photographs courtesy of Emily Photography). In exchange for the pictures, we'd love to get 1,000 words (we'll settle for your two cents -- we are a non-profit after all).

As mentioned in our most recent newsletter, we're interested in people's memories and reactions to this year's event. Any suggestions for next year's event would also be welcome including recommendations for possible nominees (though we can't promise that they'll win). Please post your responses in the comments section below!

Award Winners Past and Present

As mentioned in our most recent newsletter, we're interested in people's memories and reactions to this year's event. Any suggestions for next year's event would also be welcome including recommendations for possible nominees (though we can't promise that they'll win). Please post your responses in the comments section below!

Michael J. Sabbagh, 2010 Insurance Professional of the Year Award Winner

Name Tags

Acceptance Speech

Award Winners Past and Present

(from left to right)

Monday, November 1, 2010

Annual Meeting

Following close on the heels of the Insurance Professional of the Year Award Ceremony every year is the Annual Meeting of the Association. This year the Annual Meeting has been scheduled for Tuesday, November 16, 2010. All members of the Insurance Library are encouraged to attend (as an incentive there is a light breakfast served at 8:00am) and hear about current initiatives at the library, take a look at the library budget, and hear about new library business.

If you are a member and are unable to attend, please feel free to fill out the proxy form found here.

We hope to see you in a couple of weeks!

If you are a member and are unable to attend, please feel free to fill out the proxy form found here.

We hope to see you in a couple of weeks!

Wednesday, October 27, 2010

Products Liability Vertical File

Look two posts in one week! Remember when I said we might pop in with something brief but of interest? Here we are. The library has a number of "subject files" in our collection. These are hard copy files where we put news clippings, brochures, pamphlets etc. on various subjects related to insurance.

Today, The New York Times had an article that will likely end up in our products liability file. They also had this lovely graphic showing big settlements in drug cases:

Today, The New York Times had an article that will likely end up in our products liability file. They also had this lovely graphic showing big settlements in drug cases:

Monday, October 25, 2010

New Year's Resolution

When you're in school you follow the academic calendar, with the year starting in September. When you're in business your year starts with the new fiscal year. Here at the library, it's not official, but I feel like the year starts again after The Insurance Professional of the Year Award Ceremony is over (I might be the only one here who feels that way).

We just completed another busy start to our fall season and had a very successful (we think) event on Friday. So I feel it is time to make some new resolutions about our coming year. I vow that the library blog will no longer sit sadly neglected. We will attempt to post at least once a week, if not more.

While I cannot promise that each post will be long and descriptive, we would like to see this space be a place where we discuss current happenings at the library and in the insurance field as a whole. It might be that we just pop in and mention a great article in the New York Times that describes Insurance Exchanges (with a helpful image for clients); that we announce that the library has started an insurance fiction section (we have the entire set of Sue Grafton's Kinsey Millhone Mysteries); or we might ask you to respond with suggestions/comments on events and offerings from the library.

We just completed another busy start to our fall season and had a very successful (we think) event on Friday. So I feel it is time to make some new resolutions about our coming year. I vow that the library blog will no longer sit sadly neglected. We will attempt to post at least once a week, if not more.

While I cannot promise that each post will be long and descriptive, we would like to see this space be a place where we discuss current happenings at the library and in the insurance field as a whole. It might be that we just pop in and mention a great article in the New York Times that describes Insurance Exchanges (with a helpful image for clients); that we announce that the library has started an insurance fiction section (we have the entire set of Sue Grafton's Kinsey Millhone Mysteries); or we might ask you to respond with suggestions/comments on events and offerings from the library.

Thursday, January 14, 2010

Did You Miss Us?

The blog went on a short sabbatical last month. Between holiday closings and staff vacations, the library was busy just keeping up with requests!

Speaking of requests, The Library gets a number of interesting requests each year. We highlight some of the requests in our newsletters each quarter and provide a number of them online in our Q & A section of the website. But did you know that the library was featured in Star Magazine December 29, 1987? That's right, On the Front cover is "Jeane Dixon Predicts for 1988" and Bruce Willis and Demi Moore were hot honeymooners (not to mention Michael and Bubbles, and Charles and Di) and inside is an article entitled Wild & Wacky Insurance Claims for which we provided the fodder.

This week an instructor was asked what type of policy insured Liberace's hands and Bette Grabel's legs. He replied that it was a surplus lines policy, probably a disability policy in particular. Slate.com discussed just that three years ago when Mariah Carrey also apparently insured her legs.

Speaking of requests, The Library gets a number of interesting requests each year. We highlight some of the requests in our newsletters each quarter and provide a number of them online in our Q & A section of the website. But did you know that the library was featured in Star Magazine December 29, 1987? That's right, On the Front cover is "Jeane Dixon Predicts for 1988" and Bruce Willis and Demi Moore were hot honeymooners (not to mention Michael and Bubbles, and Charles and Di) and inside is an article entitled Wild & Wacky Insurance Claims for which we provided the fodder.

This week an instructor was asked what type of policy insured Liberace's hands and Bette Grabel's legs. He replied that it was a surplus lines policy, probably a disability policy in particular. Slate.com discussed just that three years ago when Mariah Carrey also apparently insured her legs.

Perhaps, considering all that's gone on in Haiti in the past week or so, you think this blog post is full of fluff? Maybe you'd like answers to more pressing questions? Are you wondering about insured losses in Haiti? According to a National Underwriter article citing AXCO Insurance Information Services, Haiti is "one of the smallest markets in the Americas with a total non-life premium income of just under $20 million." To put that number in perspective, total non-life direct premiums earned in the state with the lowest dpe,Vermont, is 1,094,361,000 (according to the NAIC 2008 Market Share Report by State and Countrywide) or nearly 55% more.

Insurance Journal has an article that does bring some hope to the situation, at least as far as re-building efforts. Haiti is a member of The Caribbean Catastrophe Risk Insurance Facility (CCRIF) and it appears they will give about 8 million dollars to Haiti after a 14 day waiting period so they can hurry the process of rebuilding along. National Underwriter cites Eqecat as saying the property damage is in the hundreds of millions.

Every little bit does help, though and those in the insurance industry have not neglected Haiti. According to another article by the National Underwriter, many companies have sent donations to a number of relief organizations over the last week. The Insurance Industry Charitable Foundation, gives details on at least four of the donations. The CPCU Society has also set up a matching program for individual CPCUs and Chapters of up to $25,000 for the Clinton/Bush Haiti fund.

If you'd like to contribute to help Haiti, there are many organizations out there ranging from rebuilding projects, to health and human welfare organizations, far too many to list. The FBI issued some guidlines to make sure you donate to reputable organizations.

Subscribe to:

Comments (Atom)